Introduction:

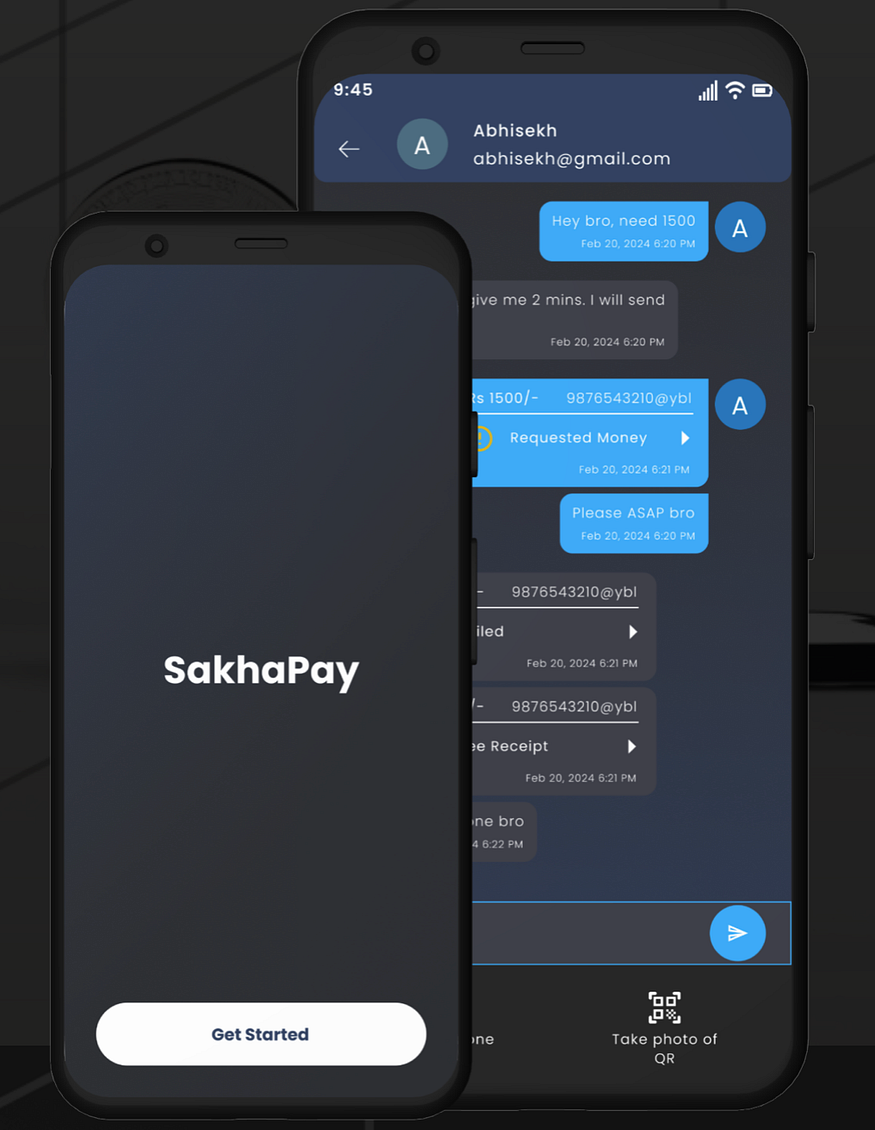

SakhaPay is an innovative payment solution targeting the Indian market. It enables collaborative payments, helping users request money through SakhaPay and then use UPI apps to initiate payments. SakhaPay also allows users to send payment receipts back through the platform, ensuring enhanced security and real-time notifications.

Understanding the User: Who Benefits from SakhaPay

- NRIs without Indian bank accounts

- Teenagers without bank accounts

- Senior citizens

- Individuals facing financial hardship

- Other users needing collaborative payment solutions

SakhaPay provides a collaborative payment solution that addresses the unique financial needs and challenges faced by these groups, offering a convenient and secure way to manage digital transactions.

Challenges:

SakhaPay stands out as an unique solution that is not yet popular in the market. It addresses a critical challenge: enabling users who are unable to make digital payments independently to seek assistance from friends or family. This feature has garnered significant attention from NRI users, highlighting its value in facilitating cross-border financial support.

Solution Development:

- User-Centric Design:

- Conducted extensive market research to understand user pain points.

- Designed an intuitive interface suitable for all age groups, from teenagers to senior citizens.

2. Feature Integration:

- Developed a built-in chat feature for smooth communication.

- Implemented receipt verification for transaction validation.

- Created IVR payment assistance to support users with limited digital literacy.

3. Security Measures:

- Ensured robust security protocols to protect user data and transactions.

- Integrated real-time alerts to keep users informed about their transactions.

4. Collaboration and Testing:

- Collaborated with engineering, design, and marketing teams for seamless development.

- Conducted beta testing with early adopters to gather feedback and make iterative improvements.

Outcomes:

SakhaPay successfully launched its beta version, achieving significant user adoption and positive feedback for its ease of use, security features, and ability to facilitate digital payments without direct bank involvement.

Conclusion:

SakhaPay’s development highlights the importance of understanding and addressing user needs through innovative and user-centric solutions. By focusing on accessibility, security, and real-time collaboration, SakhaPay has effectively catered to a diverse user base, offering a practical solution for digital payments in the Indian market.

For more information, visit SakhaPay’s website.